What is a Risk-Free Interest Rate and Why Does it Matter?

In the realm of finance, a risk-free interest rate is a crucial concept that serves as a benchmark for investments. It represents the return on an investment that carries no risk, providing a foundation for evaluating the potential risks and rewards of various investments. Understanding how to calculate risk-free interest rate is essential for investors seeking to optimize their portfolios and achieve their financial goals. By grasping this concept, investors can make more informed decisions, as it allows them to compare the expected returns of different assets and determine the required rate of return for a particular investment. In essence, the risk-free interest rate is a fundamental component of investment analysis, and its significance cannot be overstated.

Click Image to Find Quantum Products

The Role of Government Bonds in Determining the Risk-Free Rate

Government bonds, particularly those with short-term maturities, play a crucial role in estimating the risk-free interest rate. These bonds are considered to be virtually risk-free, as they are backed by the credit and taxing power of the government. As a result, they offer a relatively stable and secure return, making them an ideal proxy for the risk-free interest rate. In the United States, for example, the 3-month Treasury bill is often used as a benchmark for the risk-free interest rate. Similarly, in the European Union, the 3-month Euribor rate is used to estimate the risk-free interest rate. By analyzing the yields of these government bonds, investors can gain insight into the current market conditions and determine the required rate of return for a particular investment. Understanding how to calculate risk-free interest rate using government bonds is essential for investors seeking to make informed decisions and optimize their portfolios.

:max_bytes(150000):strip_icc()/dotdash_Final_How_Risk_Free_Is_the_Risk_Free_Rate_of_Return_Feb_2020-96f00395de3d40668f31522801756339.jpg)

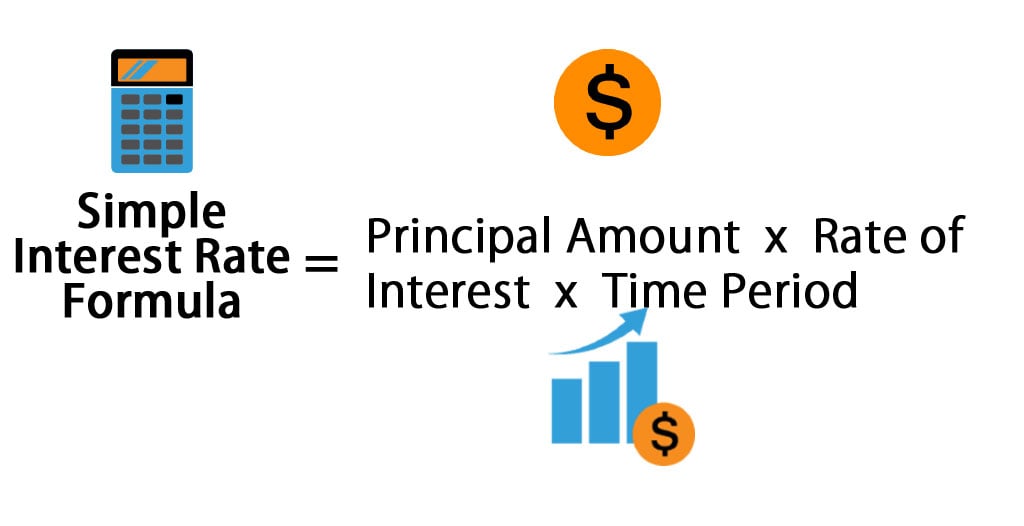

How to Calculate the Risk-Free Interest Rate: A Step-by-Step Guide

Calculating the risk-free interest rate is a crucial step in investment analysis, and it can be done using a few simple steps. The most common method is to use the yield of a short-term government bond, such as a 3-month Treasury bill. The formula to calculate the risk-free interest rate is:

Rf = (1 + (Yield / n))^(n/m) – 1

Where:

Rf = Risk-free interest rate

Yield = Yield of the short-term government bond

n = Number of times the bond compounds per year

m = Number of years until maturity

For example, if the 3-month Treasury bill has a yield of 2.5%, and it compounds quarterly, the risk-free interest rate would be:

Rf = (1 + (0.025 / 4))^(4/0.25) – 1 = 2.47%

This rate can then be used as a benchmark for evaluating the potential returns of different investments. Understanding how to calculate risk-free interest rate is essential for investors seeking to make informed decisions and optimize their portfolios. By following these simple steps, investors can gain a better understanding of the risk-free interest rate and its role in investment analysis.

:max_bytes(150000):strip_icc()/Interest-formula_5-589b8ffc5f9b58819ca83a40.jpg)

Factors Affecting the Risk-Free Interest Rate: Inflation, Economic Growth, and More

The risk-free interest rate is influenced by several key factors, including inflation, economic growth, and monetary policy. Understanding these factors is crucial for investors seeking to make informed decisions and optimize their portfolios.

Inflation is a significant factor affecting the risk-free interest rate. As inflation rises, the purchasing power of money decreases, and investors demand higher returns to compensate for the loss of value. This leads to an increase in the risk-free interest rate. For example, during periods of high inflation, central banks may increase interest rates to combat inflation, which in turn affects the risk-free interest rate.

Economic growth also plays a role in shaping the risk-free interest rate. A strong economy with high growth rates tends to lead to higher interest rates, as investors become more optimistic about the future and demand higher returns. On the other hand, a slowing economy may lead to lower interest rates, as investors become more risk-averse and seek safer investments.

Monetary policy is another key factor influencing the risk-free interest rate. Central banks, such as the Federal Reserve in the United States, set interest rates to regulate the economy and control inflation. When central banks lower interest rates, it can lead to a decrease in the risk-free interest rate, making borrowing cheaper and stimulating economic growth. Conversely, when central banks raise interest rates, it can lead to an increase in the risk-free interest rate, making borrowing more expensive and slowing down economic growth.

Other factors that can affect the risk-free interest rate include changes in government policies, global events, and market sentiment. For instance, a change in government policy, such as a tax reform, can impact the risk-free interest rate by altering the investment landscape. Similarly, global events, such as a trade war, can influence the risk-free interest rate by affecting investor confidence and market sentiment.

Understanding these factors is essential for investors seeking to calculate the risk-free interest rate accurately. By recognizing how these factors impact the rate, investors can make more informed decisions and optimize their portfolios to achieve their financial goals.

The Relationship Between Risk-Free Rate and Asset Pricing

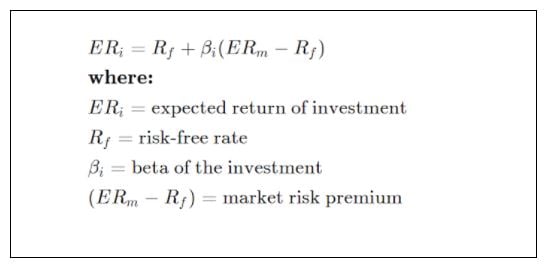

The risk-free interest rate plays a crucial role in asset pricing models, which are used to estimate the expected returns of different assets. One of the most widely used asset pricing models is the Capital Asset Pricing Model (CAPM), which relies heavily on the risk-free interest rate.

The CAPM is a linear model that describes the relationship between risk and expected return. It states that the expected return of an asset is equal to the risk-free rate plus a risk premium, which is proportional to the asset’s beta. The risk-free rate serves as a benchmark for the expected return of an asset, and the risk premium is a function of the asset’s systematic risk.

The risk-free rate is used in the CAPM to calculate the expected return of an asset. The formula for the CAPM is:

E(Ri) = Rf + βi (E(Rm) – Rf)

Where:

E(Ri) = Expected return of asset i

Rf = Risk-free interest rate

βi = Beta of asset i

E(Rm) = Expected return of the market portfolio

The risk-free rate is a critical component of the CAPM, as it provides a benchmark for the expected return of an asset. A higher risk-free rate implies a higher expected return for an asset, and vice versa. This is because investors demand a higher return for taking on more risk, and the risk-free rate represents the return of a risk-free investment.

Understanding the relationship between the risk-free rate and asset pricing is essential for investors seeking to make informed decisions. By recognizing how the risk-free rate affects the expected returns of different assets, investors can optimize their portfolios and achieve their financial goals. Furthermore, the risk-free rate serves as a benchmark for evaluating the performance of different assets, allowing investors to make more informed decisions about their investments.

Real-World Applications of the Risk-Free Interest Rate

The risk-free interest rate has numerous real-world applications in various fields, including corporate finance, portfolio management, and investment analysis. Understanding how to calculate the risk-free interest rate is essential for making informed investment decisions and achieving financial goals.

In corporate finance, the risk-free interest rate is used to evaluate investment opportunities and determine the cost of capital. For instance, a company may use the risk-free rate to calculate the net present value (NPV) of a project, which helps to determine whether the project is profitable or not. A higher risk-free rate may indicate that a project is not viable, while a lower rate may suggest that it is a good investment opportunity.

In portfolio management, the risk-free interest rate is used to construct optimal portfolios that balance risk and return. Portfolio managers use the risk-free rate as a benchmark to evaluate the performance of different assets and determine the optimal asset allocation. For example, a portfolio manager may use the risk-free rate to calculate the expected return of a stock and determine whether it is overvalued or undervalued.

In investment analysis, the risk-free interest rate is used to evaluate the performance of different investments, such as stocks, bonds, and mutual funds. Investment analysts use the risk-free rate to calculate the excess return of an investment, which is the return above the risk-free rate. This helps to determine whether an investment is generating sufficient returns to justify the risk taken.

Additionally, the risk-free interest rate is used in other areas, such as in the calculation of the cost of equity, the evaluation of derivatives, and the determination of the yield curve. Understanding how to calculate the risk-free interest rate is essential for making informed investment decisions and achieving financial goals.

By recognizing the real-world applications of the risk-free interest rate, investors can gain a deeper understanding of how to calculate this rate and make more informed investment decisions. Whether in corporate finance, portfolio management, or investment analysis, the risk-free interest rate plays a critical role in evaluating investment opportunities and achieving financial goals.

Common Mistakes to Avoid When Calculating the Risk-Free Interest Rate

When calculating the risk-free interest rate, investors often encounter common mistakes or misconceptions that can lead to inaccurate results. Understanding these pitfalls is crucial to avoid errors and make informed investment decisions.

One common mistake is using the wrong type of government bond to estimate the risk-free rate. For instance, using long-term government bonds instead of short-term bonds can lead to an inaccurate calculation. It is essential to use short-term government bonds with maturities of less than one year to estimate the risk-free rate.

Another mistake is failing to consider the credit risk of government bonds. Although government bonds are considered to be risk-free, they still carry some credit risk. Investors should use bonds with the highest credit rating to minimize credit risk and ensure an accurate calculation.

Additionally, investors may overlook the impact of inflation on the risk-free interest rate. Inflation can erode the purchasing power of investments, and failing to account for it can lead to an inaccurate calculation. Investors should use inflation-indexed bonds or adjust the risk-free rate for inflation to ensure an accurate calculation.

Furthermore, investors may use outdated or incorrect data to calculate the risk-free interest rate. It is essential to use current and reliable data to ensure an accurate calculation. Investors can use financial databases or websites to access current data on government bond yields.

To avoid these common mistakes, investors should follow a step-by-step approach to calculating the risk-free interest rate. This includes selecting the right type of government bond, considering credit risk, accounting for inflation, and using current and reliable data. By avoiding these common mistakes, investors can ensure an accurate calculation of the risk-free interest rate and make informed investment decisions.

By understanding how to calculate the risk-free interest rate and avoiding common mistakes, investors can gain a deeper understanding of this critical concept and make more informed decisions. Whether in corporate finance, portfolio management, or investment analysis, the risk-free interest rate plays a vital role in evaluating investment opportunities and achieving financial goals.

Conclusion: Mastering the Risk-Free Interest Rate for Informed Investment Decisions

In conclusion, understanding the risk-free interest rate and how to calculate it is crucial for investors seeking to make informed decisions. The risk-free rate serves as a benchmark for investments, providing a basis for evaluating the performance of different assets. By grasping the concepts outlined in this guide, investors can gain a deeper understanding of how to calculate the risk-free interest rate and avoid common mistakes.

Mastering the risk-free interest rate is essential for achieving financial goals, whether in corporate finance, portfolio management, or investment analysis. By recognizing the significance of this rate, investors can make more informed decisions and optimize their investment portfolios. Remember, understanding how to calculate the risk-free interest rate is a critical step in unlocking the secrets of risk-free investing.

By following the step-by-step guide outlined in this article, investors can accurately calculate the risk-free interest rate and make informed decisions. It is essential to consider the factors that influence the risk-free rate, such as inflation, economic growth, and monetary policy, to ensure an accurate calculation. Additionally, investors should avoid common mistakes, such as using the wrong type of government bond or failing to account for inflation.

In today’s complex financial landscape, understanding how to calculate the risk-free interest rate is more important than ever. By mastering this critical concept, investors can navigate the markets with confidence and achieve their financial goals. Whether you are a seasoned investor or just starting out, grasping the risk-free interest rate is essential for success in the world of finance.