What Drives the Equity Risk Premium: Understanding the Fundamentals

In the pursuit of optimal investment returns, understanding the equity risk premium is crucial. Calculating the equity risk premium is a vital step in determining the expected return on investment, as it represents the excess return investors demand for taking on the risk of investing in the stock market. The equity risk premium is influenced by a multitude of factors, including market volatility, economic growth, and investor sentiment. Market volatility, for instance, can significantly impact the equity risk premium, as investors tend to demand higher returns during periods of high uncertainty. Economic growth, on the other hand, can lead to increased investor confidence, resulting in a lower equity risk premium. Investor sentiment, which can be influenced by various market and economic factors, also plays a significant role in shaping the equity risk premium. By grasping these fundamental factors, investors can better understand the equity risk premium and make informed decisions about their investments.

Click Image to Find Quantum Products

How to Calculate the Equity Risk Premium: A Step-by-Step Approach

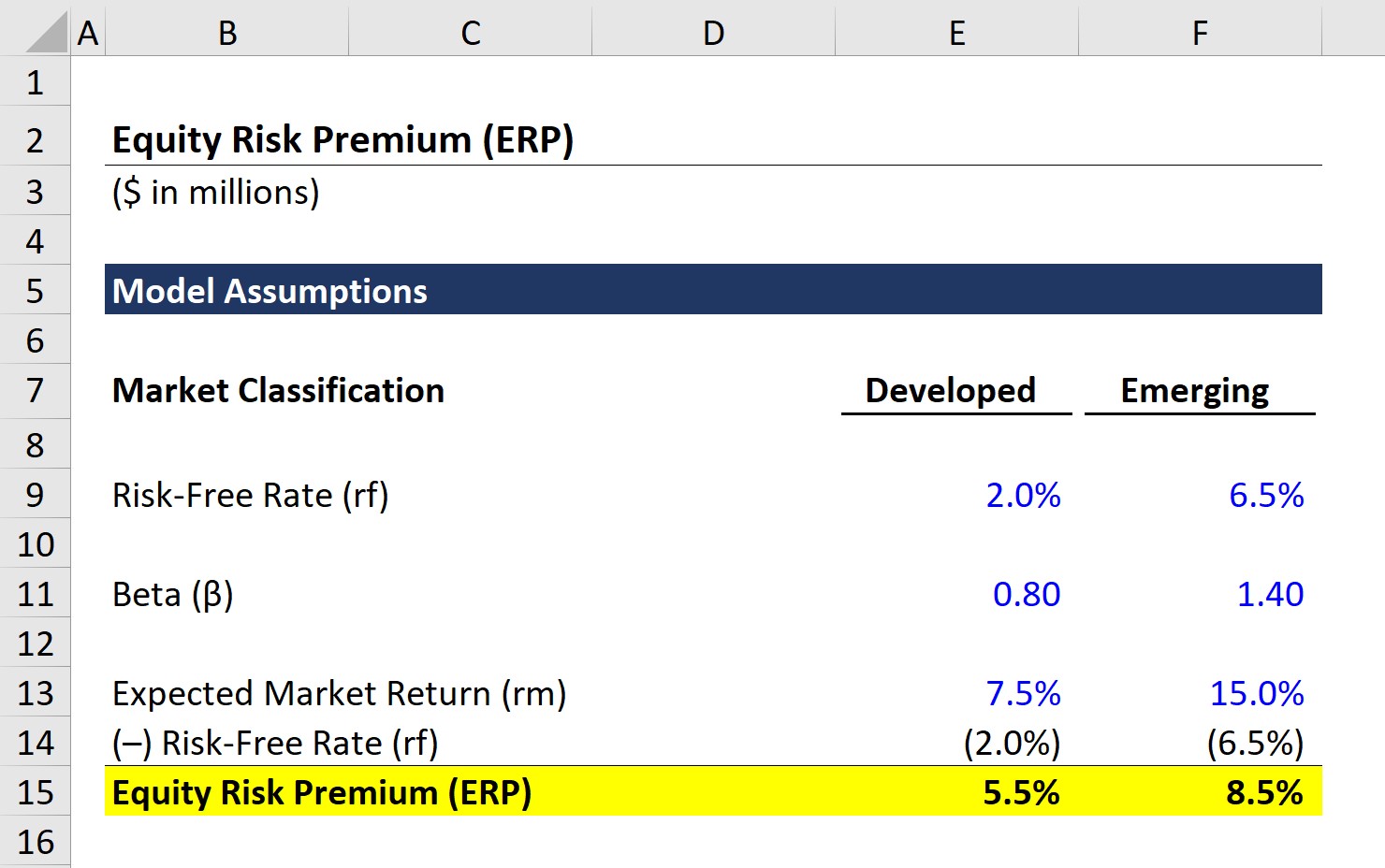

Calculating the equity risk premium is a crucial step in investment decisions, as it helps investors determine the expected return on investment. There are several methods and formulas used to calculate the equity risk premium, each with its own strengths and limitations. One of the most widely used methods is the Capital Asset Pricing Model (CAPM), which estimates the equity risk premium based on the market return, risk-free rate, and beta of the asset. The Arbitrage Pricing Theory (APT) is another popular method, which takes into account multiple factors that affect the equity risk premium. To calculate the equity risk premium using these methods, investors need to follow a step-by-step approach. First, they need to determine the market return and risk-free rate. Next, they need to estimate the beta of the asset, which can be done using historical data or industry averages. Finally, they can plug in these values into the CAPM or APT formulas to calculate the equity risk premium. By following this step-by-step approach, investors can accurately calculate the equity risk premium and make informed investment decisions. Additionally, understanding the different methods and formulas used in calculating the equity risk premium can help investors optimize their investment portfolios and manage risk more effectively.

The Role of Historical Data in Estimating the Equity Risk Premium

Historical data plays a crucial role in estimating the equity risk premium, as it provides valuable insights into the behavior of the stock market over time. One of the most common approaches to estimating the equity risk premium is to use long-term averages of historical data. This involves calculating the average return of the stock market over a long period, typically 10-20 years, and using this value as an estimate of the equity risk premium. However, relying solely on historical data has its limitations. For instance, past performance is not always a guarantee of future results, and the stock market can be affected by a wide range of factors that are difficult to predict. Additionally, historical data may not capture rare events or black swans that can have a significant impact on the stock market. Therefore, it is essential to combine historical data with other approaches, such as econometric models and machine learning algorithms, to obtain a more accurate estimate of the equity risk premium. By doing so, investors can gain a better understanding of the equity risk premium and make more informed investment decisions. Furthermore, calculating the equity risk premium using historical data can help investors identify trends and patterns in the stock market, which can be used to optimize investment portfolios and manage risk more effectively.

Debunking Common Myths About the Equity Risk Premium

When it comes to calculating the equity risk premium, there are several common misconceptions that can lead to inaccurate estimates and poor investment decisions. One of the most prevalent myths is that the equity risk premium is always positive. However, this is not necessarily the case. In times of high market volatility or economic uncertainty, the equity risk premium can be negative, indicating that investors are willing to accept lower returns in exchange for reduced risk. Another myth is that the equity risk premium is constant over time, when in fact it can vary significantly depending on market conditions and macroeconomic factors. For instance, during periods of high inflation, the equity risk premium may increase as investors demand higher returns to compensate for the erosion of purchasing power. By understanding these common myths and misconceptions, investors can avoid making costly mistakes and develop a more accurate and nuanced understanding of the equity risk premium. This, in turn, can help them make more informed investment decisions and optimize their portfolios for better returns. Calculating the equity risk premium requires a thorough understanding of these complexities and a willingness to challenge common myths and assumptions.

The Impact of Macroeconomic Factors on the Equity Risk Premium

Macroeconomic factors play a crucial role in shaping the equity risk premium, and understanding their impact is essential for accurately calculating the equity risk premium. Inflation, for instance, can have a significant influence on the equity risk premium. During periods of high inflation, investors may demand higher returns to compensate for the erosion of purchasing power, leading to an increase in the equity risk premium. On the other hand, low inflation or deflationary environments may lead to lower equity risk premiums as investors are willing to accept lower returns in exchange for reduced risk. Interest rates also have a profound impact on the equity risk premium. When interest rates are high, investors may prefer fixed-income investments over equities, leading to a decrease in the equity risk premium. Conversely, low interest rates may lead to an increase in the equity risk premium as investors seek higher returns in the equity market. GDP growth is another key macroeconomic factor that can influence the equity risk premium. During periods of strong economic growth, investors may be more willing to take on risk, leading to a decrease in the equity risk premium. In contrast, slow economic growth or recessions may lead to an increase in the equity risk premium as investors become more risk-averse. By understanding the complex relationships between these macroeconomic factors and the equity risk premium, investors can make more informed investment decisions and develop more accurate estimates of the equity risk premium. Calculating the equity risk premium requires a deep understanding of these macroeconomic factors and their impact on investor behavior and market dynamics.

Comparing Different Approaches to Estimating the Equity Risk Premium

Estimating the equity risk premium is a complex task that requires a deep understanding of various approaches and methods. There are several ways to estimate the equity risk premium, each with its strengths and limitations. One approach is to use surveys, which involve collecting data from investors and financial professionals to estimate the equity risk premium. This method can provide valuable insights into market sentiment and investor expectations. Another approach is to use econometric models, such as the Capital Asset Pricing Model (CAPM) and the Arbitrage Pricing Theory (APT), which rely on historical data and mathematical formulas to estimate the equity risk premium. These models can provide a more objective estimate of the equity risk premium, but may be limited by their reliance on historical data. More recently, machine learning algorithms have been applied to estimating the equity risk premium, using large datasets and complex models to identify patterns and relationships. This approach can provide more accurate and reliable estimates, but may be limited by the quality and availability of data. By comparing and contrasting these different approaches, investors can gain a deeper understanding of the equity risk premium and develop more accurate estimates. Calculating the equity risk premium requires a thorough understanding of these different approaches and their limitations, as well as the ability to adapt to changing market conditions and investor sentiment. By combining these approaches and incorporating new data and methods, investors can develop more accurate and reliable estimates of the equity risk premium, ultimately leading to better investment decisions and more effective portfolio management.

Practical Applications of the Equity Risk Premium in Portfolio Management

The equity risk premium plays a crucial role in portfolio management, as it helps investors and portfolio managers make informed investment decisions and manage risk. By understanding the equity risk premium, investors can optimize their investment portfolios to achieve their desired level of risk and return. For instance, investors with a higher risk tolerance may choose to invest in stocks with a higher equity risk premium, while those with a lower risk tolerance may opt for bonds or other fixed-income investments with a lower equity risk premium. Calculating the equity risk premium is essential in this process, as it allows investors to quantify the potential returns and risks associated with different investments. Furthermore, the equity risk premium can be used to manage risk by diversifying portfolios and allocating assets effectively. By incorporating the equity risk premium into their investment decisions, investors can create more efficient portfolios that balance risk and return. Additionally, the equity risk premium can be used to evaluate the performance of investment managers and portfolios, providing a benchmark for assessing investment decisions. Overall, the equity risk premium is a critical component of portfolio management, and understanding how to calculate and apply it is essential for achieving investment success. By mastering the art of calculating the equity risk premium, investors can unlock the secrets of investment returns and make more informed investment decisions.

:max_bytes(150000):strip_icc()/dotdash_Final_Calculating_the_Equity_Risk_Premium_Dec_2020-01-1ff6e59964b9408d9ac7d175f8ad1292.jpg)

Future Directions: Advancements in Estimating the Equity Risk Premium

The field of estimating the equity risk premium is constantly evolving, with new approaches and methodologies being developed to improve the accuracy and reliability of estimates. One promising area of research is the use of alternative data sources, such as big data and machine learning algorithms, to estimate the equity risk premium. These approaches have the potential to provide more accurate and reliable estimates by incorporating a wider range of data and variables. For example, machine learning algorithms can be used to analyze large datasets and identify patterns and relationships that may not be apparent through traditional methods. Additionally, the use of big data can provide a more comprehensive understanding of market trends and investor sentiment, allowing for more accurate estimates of the equity risk premium. Furthermore, the increasing availability of data and advances in computing power are enabling researchers to develop more sophisticated models and methods for calculating the equity risk premium. As these approaches continue to evolve, they have the potential to revolutionize the field of estimating the equity risk premium, providing investors and portfolio managers with more accurate and reliable estimates. By staying at the forefront of these developments, investors can gain a competitive edge in calculating the equity risk premium and making informed investment decisions. As the field continues to evolve, it is likely that new and innovative approaches will emerge, providing even more accurate and reliable estimates of the equity risk premium.