What is Equity Risk Premium and Why Does it Matter?

In the realm of finance, equity risk premium plays a pivotal role in investment decisions. It represents the excess return an investor can expect from holding a risky asset, such as stocks, over a risk-free asset, like government bonds. This premium is a compensation for taking on additional risk, and it significantly affects portfolio returns. In today’s volatile market, understanding equity risk premium is crucial, as it can help investors make informed decisions about their investments and manage risk more effectively. By grasping the concept of equity risk premium, investors can better navigate the complexities of the market and make more informed decisions about their investments. As investors seek to maximize returns while minimizing risk, understanding how to calculate equity risk premium becomes essential. In this article, we will delve into the intricacies of equity risk premium, exploring its components, calculation methods, and real-world applications.

Click Image to Find Quantum Products

Understanding the Components of Equity Risk Premium

Equity risk premium is a multifaceted concept, comprising three primary components: the risk-free rate, market return, and beta. Each of these components plays a crucial role in determining the overall equity risk premium. The risk-free rate represents the return on a risk-free investment, such as government bonds, and serves as a benchmark for other investments. The market return, on the other hand, is the average return of the overall market, and it reflects the performance of the broader economy. Beta, a measure of systematic risk, gauges the volatility of an individual stock or portfolio relative to the market as a whole. By understanding how these components interact and contribute to the equity risk premium, investors can better appreciate the complexities of the market and make more informed investment decisions. For instance, a stock with a high beta will generally have a higher equity risk premium, as it is more volatile and therefore riskier. Conversely, a stock with a low beta will have a lower equity risk premium, as it is less volatile and therefore less risky. As investors seek to maximize returns while minimizing risk, grasping the components of equity risk premium is essential. In the next section, we will explore how to calculate equity risk premium using the Capital Asset Pricing Model (CAPM), a widely-used framework for estimating equity risk premium.

The Capital Asset Pricing Model (CAPM): A Framework for Calculating Equity Risk Premium

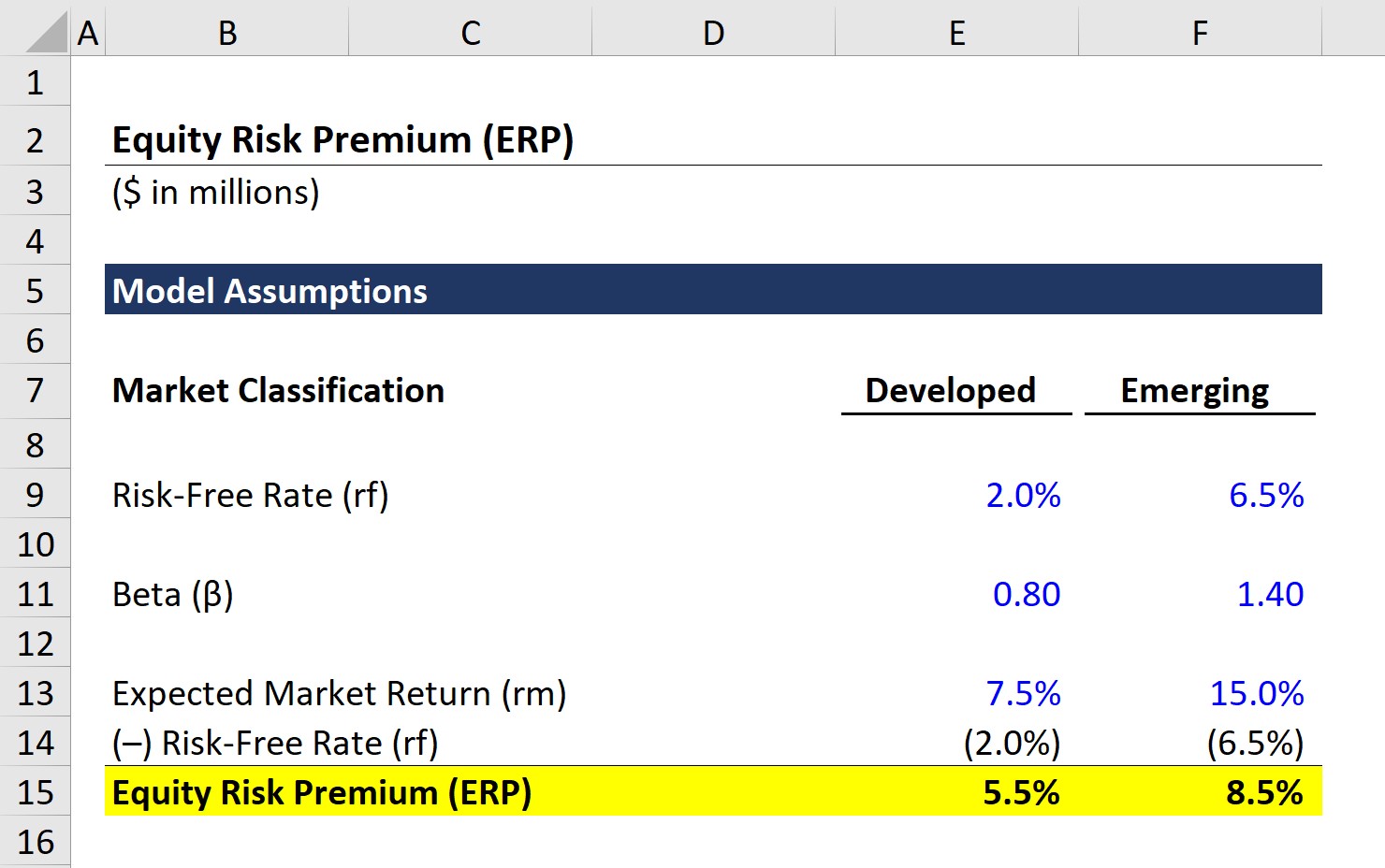

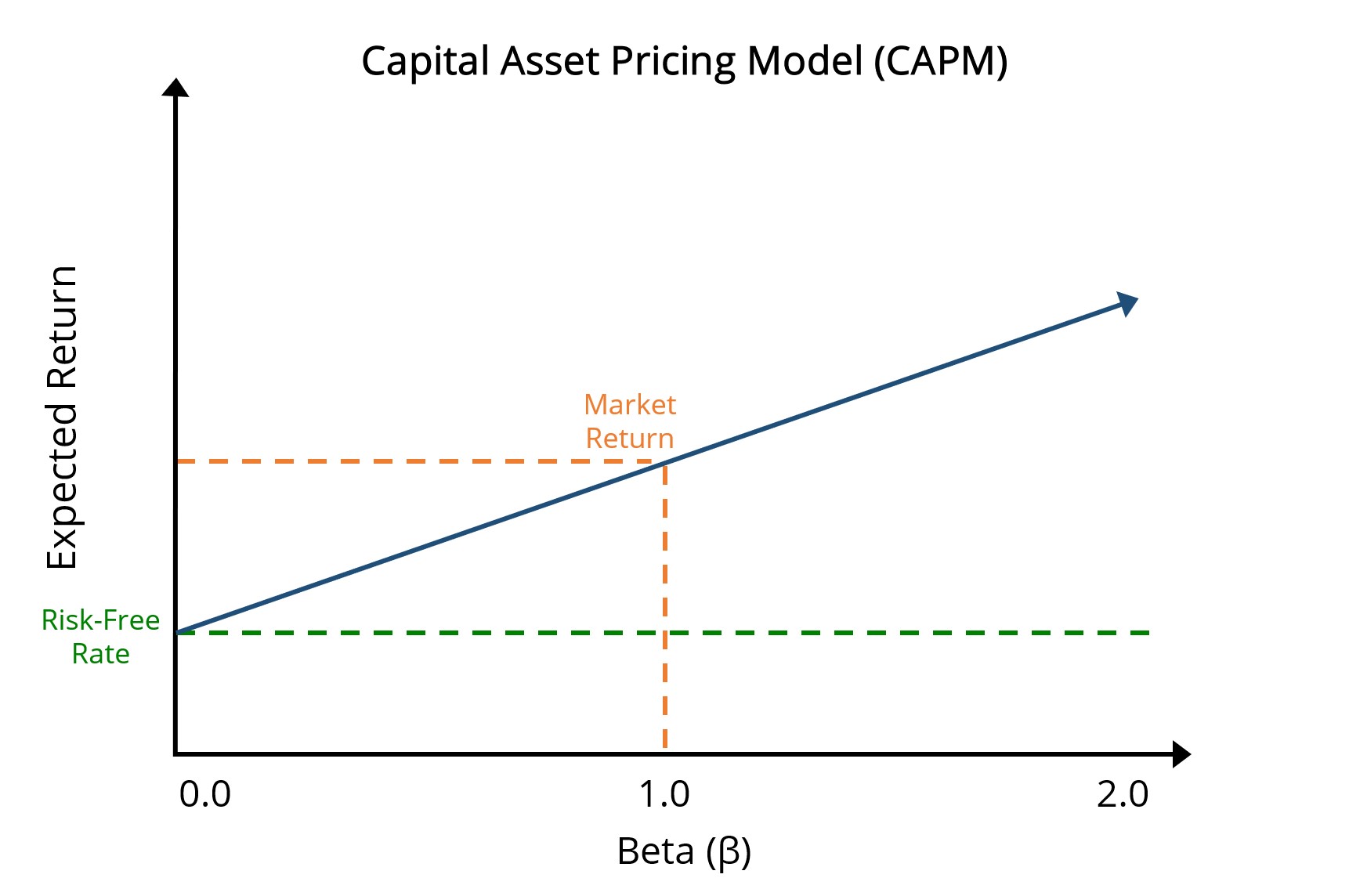

The Capital Asset Pricing Model (CAPM) is a widely-used framework for calculating equity risk premium. Developed by William Sharpe in the 1960s, CAPM provides a systematic approach to estimating the expected return on an investment based on its beta and the risk-free rate. The CAPM formula is: Expected Return = Risk-Free Rate + Beta \* (Market Return – Risk-Free Rate). This formula takes into account the risk-free rate, market return, and beta to estimate the expected return on an investment. By using CAPM, investors can calculate the equity risk premium, which represents the excess return an investment is expected to generate over the risk-free rate. CAPM assumes that investors are rational and that markets are efficient, which means that prices reflect all available information. While CAPM has its limitations, such as assuming a normal distribution of returns, it remains a widely-used and influential model in finance. In the next section, we will provide a step-by-step guide on how to calculate equity risk premium using CAPM, including examples and formulas. Understanding how to calculate equity risk premium is crucial, as it can help investors make informed decisions about their investments and manage risk more effectively. By grasping the concepts of CAPM and equity risk premium, investors can better navigate the complexities of the market and achieve their investment goals.

How to Calculate Equity Risk Premium: A Step-by-Step Guide

To calculate equity risk premium, investors can use the Capital Asset Pricing Model (CAPM) formula: Expected Return = Risk-Free Rate + Beta \* (Market Return – Risk-Free Rate). This formula requires three inputs: the risk-free rate, market return, and beta. Here’s a step-by-step guide on how to calculate equity risk premium using CAPM:

Step 1: Determine the risk-free rate, which is typically the yield on a long-term government bond, such as the 10-year Treasury bond.

Step 2: Estimate the market return, which can be based on historical data or forward-looking expectations. A common approach is to use the average annual return of a broad market index, such as the S&P 500.

Step 3: Calculate the beta of the investment, which measures its systematic risk relative to the market. Beta can be estimated using historical data or obtained from financial databases.

Step 4: Plug in the values into the CAPM formula to estimate the expected return on the investment.

For example, let’s say the risk-free rate is 2%, the market return is 8%, and the beta of the investment is 1.2. Using the CAPM formula, the expected return would be: Expected Return = 2% + 1.2 \* (8% – 2%) = 9.6%.

It’s essential to use historical data and adjust for inflation when calculating equity risk premium. This ensures that the estimates are based on realistic expectations and reflect the actual performance of the market. By following these steps, investors can accurately calculate equity risk premium and make informed investment decisions. Remember, how do you calculate equity risk premium is a crucial question in finance, and understanding the answer can help investors achieve their investment goals.

Common Pitfalls to Avoid When Calculating Equity Risk Premium

When calculating equity risk premium, investors must be aware of common pitfalls that can lead to inaccurate estimates. These mistakes can have significant implications for investment decisions, as they can result in mispriced assets and suboptimal portfolio construction. Here are some common mistakes to avoid:

Incorrect Data: Using outdated or incorrect data can lead to flawed estimates of equity risk premium. Investors must ensure that they are using reliable and up-to-date data sources, such as historical market returns and risk-free rates.

Ignoring Inflation: Failing to adjust for inflation can result in underestimated equity risk premiums. Investors must account for inflation when calculating historical market returns and risk-free rates to ensure accurate estimates.

Overlooking Beta: Beta is a critical component of equity risk premium, and overlooking it can lead to inaccurate estimates. Investors must ensure that they are using accurate beta estimates, which can be obtained from financial databases or calculated using historical data.

Assuming Constant Risk Premium: Equity risk premium can vary over time, and assuming a constant risk premium can lead to inaccurate estimates. Investors must be aware of changes in market conditions and adjust their estimates accordingly.

By avoiding these common pitfalls, investors can ensure accurate calculations of equity risk premium and make informed investment decisions. Remember, how do you calculate equity risk premium is a crucial question in finance, and understanding the answer can help investors achieve their investment goals. By being aware of these common mistakes, investors can avoid costly errors and optimize their investment strategies.

Real-World Applications of Equity Risk Premium in Investment Decisions

In the world of finance, equity risk premium plays a critical role in informing investment decisions. By accurately calculating equity risk premium, investors can optimize their portfolios, allocate assets effectively, and manage risk. Here are some real-world applications of equity risk premium in investment decisions:

Portfolio Optimization: Equity risk premium is used to determine the optimal mix of assets in a portfolio. By estimating the expected returns and risks of different assets, investors can create a diversified portfolio that maximizes returns while minimizing risk.

Asset Allocation: Equity risk premium helps investors allocate assets across different classes, such as stocks, bonds, and real estate. By understanding the risk premium associated with each asset class, investors can allocate their assets effectively and achieve their investment goals.

Risk Management: Equity risk premium is essential for managing risk in investment portfolios. By understanding the risk premium associated with different assets, investors can identify potential risks and take steps to mitigate them.

For example, an investor may use equity risk premium to determine the expected return on a stock investment. If the expected return is higher than the risk-free rate, the investor may decide to invest in the stock. On the other hand, if the expected return is lower than the risk-free rate, the investor may decide to avoid the investment.

In another example, a portfolio manager may use equity risk premium to optimize a portfolio of stocks and bonds. By estimating the risk premium associated with each asset, the portfolio manager can create a diversified portfolio that maximizes returns while minimizing risk.

By understanding how to calculate equity risk premium and its applications in investment decisions, investors can make informed decisions that drive long-term success. Remember, how do you calculate equity risk premium is a crucial question in finance, and understanding the answer can help investors achieve their investment goals.

/dotdash_Final_Calculating_the_Equity_Risk_Premium_Dec_2020-01-1ff6e59964b9408d9ac7d175f8ad1292.jpg)

Alternative Approaches to Calculating Equity Risk Premium

In addition to the Capital Asset Pricing Model (CAPM), there are alternative approaches to calculating equity risk premium. These approaches provide different perspectives on how to estimate equity risk premium and can be useful in certain situations.

The Fama-French Three-Factor Model: This model, developed by Eugene Fama and Kenneth French, expands on the CAPM by including two additional factors: size and value. The model recognizes that small-cap and value stocks tend to have higher returns than large-cap and growth stocks, and therefore, require a higher risk premium.

The Arbitrage Pricing Theory (APT): Developed by Stephen Ross, APT is a multifactor model that estimates equity risk premium based on a range of macroeconomic factors, such as inflation, GDP, and interest rates. APT provides a more comprehensive approach to estimating equity risk premium by considering multiple factors that affect asset returns.

Other approaches, such as the conditional CAPM and the Bayesian approach, also exist. These approaches offer different ways to estimate equity risk premium and can be useful in certain situations, such as when dealing with non-normal distributions or incomplete data.

Each alternative approach has its advantages and limitations. For example, the Fama-French three-factor model is more comprehensive than CAPM but requires more data and is more complex to implement. APT, on the other hand, is more flexible but requires a deeper understanding of macroeconomic factors.

Understanding these alternative approaches can help investors and analysts make more informed decisions when calculating equity risk premium. By recognizing the strengths and weaknesses of each approach, investors can choose the most suitable method for their specific needs and goals. Remember, how do you calculate equity risk premium is a crucial question in finance, and understanding the different approaches can help investors achieve their investment goals.

Conclusion: Mastering the Art of Equity Risk Premium Calculation

In conclusion, accurately calculating equity risk premium is crucial for informed investment decisions. By understanding the components of equity risk premium, the Capital Asset Pricing Model (CAPM), and alternative approaches, investors can make more informed decisions about their portfolios. Remember, how do you calculate equity risk premium is a critical question in finance, and mastering this concept can help investors achieve their investment goals.

In today’s volatile market, understanding equity risk premium is more important than ever. By recognizing the significance of equity risk premium, investors can optimize their portfolios, manage risk, and maximize returns. Whether you’re a seasoned investor or just starting out, grasping the concept of equity risk premium can help you make more informed investment decisions.

In this comprehensive guide, we’ve covered the essential concepts and approaches to calculating equity risk premium. From the basics of CAPM to alternative approaches, we’ve provided a step-by-step guide to help investors master the art of equity risk premium calculation. By applying these concepts, investors can unlock the secrets of equity risk premium and make more informed investment decisions.

Ultimately, accurately calculating equity risk premium is key to achieving long-term investment success. By understanding how to calculate equity risk premium, investors can navigate the complexities of the market and make informed decisions that drive results. Whether you’re a professional investor or an individual investor, mastering the art of equity risk premium calculation can help you achieve your investment goals and succeed in today’s fast-paced financial landscape.

:max_bytes(150000):strip_icc()/dotdash_Final_Calculating_the_Equity_Risk_Premium_Dec_2020-06-acd73a07b27f4ea38d124481e271fe49.jpg)