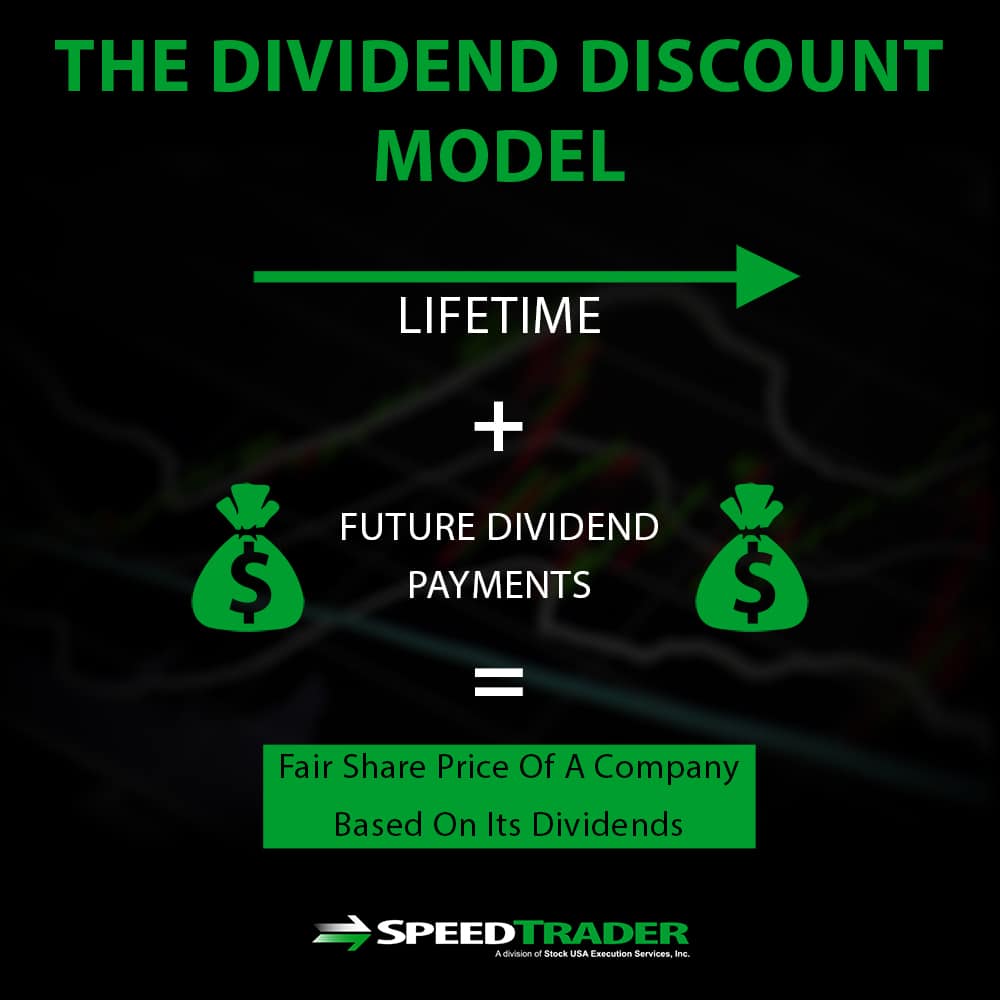

Understanding the Dividend Discount Model

In the realm of dividend investing, the dividend discount model (DDM) is a widely recognized valuation technique that enables investors to estimate the intrinsic value of a stock. By discounting the expected future dividend payments to their present value, the DDM provides a framework for evaluating the potential return on investment of a dividend-paying stock. This model is particularly useful for investors seeking to make informed investment decisions, as it helps to identify undervalued or overvalued stocks. The DDM is a fundamental concept in dividend investing, and its variations, such as the 2-stage dividend discount model, offer even more sophisticated approaches to stock valuation.

Click Image to Find Quantum Products

What is the 2-Stage Dividend Discount Model?

The 2-stage dividend discount model is a variation of the traditional dividend discount model, offering a more sophisticated approach to stock valuation. This model assumes that a company’s dividend growth rate will undergo a transition from a high-growth phase to a stable growth phase. The 2-stage dividend discount model is particularly useful for companies experiencing rapid growth, as it captures the complexities of dividend growth more accurately than the traditional model. By acknowledging the different growth phases, investors can make more informed investment decisions, as the model provides a more realistic estimate of the stock’s intrinsic value.

How to Apply the 2-Stage Dividend Discount Model in Practice

To apply the 2-stage dividend discount model, investors must follow a step-by-step approach. The first step is to estimate the cost of capital, which represents the expected return on investment. This can be done using the capital asset pricing model (CAPM) or other methods. Next, investors must estimate the dividend growth rates for both the high-growth and stable growth phases. This can be achieved by analyzing historical dividend data, industry trends, and company-specific factors. The terminal value, which represents the present value of future dividend payments, must also be estimated. This can be done using the perpetuity growth model or other methods.

Once these inputs are estimated, investors can plug them into the 2-stage dividend discount model formula. The formula takes into account the present value of dividend payments during the high-growth phase, the present value of dividend payments during the stable growth phase, and the terminal value. By calculating the intrinsic value of the stock using the 2-stage dividend discount model, investors can compare it to the current market price and make informed investment decisions.

For example, let’s say an investor is analyzing a company with a high-growth phase dividend growth rate of 10% and a stable growth phase dividend growth rate of 5%. The cost of capital is estimated to be 8%, and the terminal value is estimated to be $50. Using the 2-stage dividend discount model formula, the investor calculates the intrinsic value of the stock to be $75. If the current market price is $60, the investor may consider the stock to be undervalued and a potential investment opportunity.

Estimating Dividend Growth Rates: A Critical Component

Accurately estimating dividend growth rates is a critical component of the 2-stage dividend discount model. Dividend growth rates have a significant impact on the intrinsic value of a stock, and small errors in estimation can lead to large differences in valuation. To estimate dividend growth rates, investors can analyze historical dividend data, industry trends, and company-specific factors.

Historical dividend data can provide valuable insights into a company’s dividend payment patterns. Investors can analyze the company’s dividend payout ratio, dividend yield, and dividend growth rate over time to identify trends and patterns. Industry trends can also be analyzed to determine if the company’s dividend growth rate is in line with industry averages.

Company-specific factors, such as the company’s business model, competitive advantage, and management’s dividend policy, can also be analyzed to estimate dividend growth rates. For example, a company with a strong competitive advantage and a history of increasing dividend payments may be expected to have a higher dividend growth rate than a company with a weaker competitive position.

In addition to these factors, investors can also use quantitative models, such as the Gordon Growth Model, to estimate dividend growth rates. The Gordon Growth Model assumes that dividend growth rates will slow down over time, eventually reaching a stable growth rate. By using this model, investors can estimate the dividend growth rate during the high-growth phase and the stable growth phase of the 2-stage dividend discount model.

By accurately estimating dividend growth rates, investors can increase the accuracy of the 2-stage dividend discount model and make more informed investment decisions. The 2-stage dividend discount model is a powerful tool for estimating the intrinsic value of a stock, and accurate estimation of dividend growth rates is critical to its success.

:max_bytes(150000):strip_icc()/dividendgrowthrate-final-b83e22b0413c454aa4083ec89f65c1b8.jpg)

Case Study: Applying the 2-Stage Dividend Discount Model to a Real-World Example

To illustrate the application of the 2-stage dividend discount model, let’s consider a real-world example. Suppose we want to estimate the intrinsic value of a stock, XYZ Inc., which has a history of paying consistent dividends. We will use the 2-stage dividend discount model to estimate the intrinsic value of XYZ Inc.

First, we need to estimate the cost of capital, which represents the expected return on investment. Using the capital asset pricing model (CAPM), we estimate the cost of capital to be 9%. Next, we need to estimate the dividend growth rates for both the high-growth and stable growth phases. After analyzing historical dividend data and industry trends, we estimate the high-growth phase dividend growth rate to be 12% and the stable growth phase dividend growth rate to be 6%.

We also need to estimate the terminal value, which represents the present value of future dividend payments. Using the perpetuity growth model, we estimate the terminal value to be $40. Finally, we can plug in these inputs into the 2-stage dividend discount model formula to estimate the intrinsic value of XYZ Inc.

Using the 2-stage dividend discount model, we calculate the intrinsic value of XYZ Inc. to be $65. If the current market price is $55, we may consider the stock to be undervalued and a potential investment opportunity. The 2-stage dividend discount model provides a more accurate estimate of the intrinsic value of XYZ Inc. by capturing the complexities of dividend growth.

This case study demonstrates the application of the 2-stage dividend discount model in practice. By following a step-by-step approach, investors can estimate the intrinsic value of a stock using the 2-stage dividend discount model. The model provides a powerful tool for making informed investment decisions and can be applied to a wide range of dividend-paying stocks.

Limitations and Potential Biases of the 2-Stage Dividend Discount Model

The 2-stage dividend discount model is a powerful tool for estimating the intrinsic value of a stock, but it is not without its limitations and potential biases. One of the main limitations of the model is the assumption of constant growth rates during the high-growth and stable growth phases. In reality, dividend growth rates can be volatile and may not follow a consistent pattern.

Another potential bias of the 2-stage dividend discount model is the impact of external factors on dividend payments. For example, changes in interest rates, economic conditions, or regulatory environments can affect a company’s ability to pay dividends. The model assumes that these external factors will not significantly impact dividend payments, which may not always be the case.

Additionally, the 2-stage dividend discount model relies on estimates of the cost of capital, dividend growth rates, and terminal value, which can be subject to errors and biases. Small errors in these estimates can lead to large differences in the estimated intrinsic value of a stock.

Furthermore, the 2-stage dividend discount model is based on the assumption that the stock market is efficient and that prices reflect all available information. However, in reality, markets can be inefficient, and prices may not always reflect the true value of a stock.

Despite these limitations and potential biases, the 2-stage dividend discount model remains a useful tool for investors. By understanding the limitations of the model, investors can use it in conjunction with other valuation methods to make more informed investment decisions. The 2-stage dividend discount model can provide valuable insights into the intrinsic value of a stock, but it should be used with caution and in conjunction with other analytical tools.

Comparing the 2-Stage Dividend Discount Model with Other Valuation Methods

When it comes to estimating the intrinsic value of a stock, investors have a range of valuation methods at their disposal. In this section, we’ll compare the 2-stage dividend discount model with other popular valuation methods, including the discounted cash flow (DCF) model and the capital asset pricing model (CAPM).

The DCF model is a widely used valuation method that estimates the present value of a company’s future cash flows. While the DCF model is similar to the 2-stage dividend discount model in that it estimates the present value of future cash flows, it differs in that it focuses on cash flows rather than dividend payments. The DCF model is particularly useful for companies with irregular dividend payments or those that retain a significant portion of their earnings.

The CAPM, on the other hand, is a valuation method that estimates the expected return on investment based on the company’s beta, the risk-free rate, and the market return. While the CAPM is not a direct valuation method, it can be used in conjunction with the 2-stage dividend discount model to estimate the cost of capital.

In comparison to the DCF model, the 2-stage dividend discount model is more suitable for companies with a consistent dividend payment history. The 2-stage dividend discount model is also more straightforward to apply, as it requires fewer inputs than the DCF model. However, the DCF model provides a more comprehensive picture of a company’s cash flows and can be more accurate for companies with complex cash flow profiles.

In comparison to the CAPM, the 2-stage dividend discount model provides a more direct estimate of the intrinsic value of a stock. The CAPM, on the other hand, provides an estimate of the expected return on investment, which can be used to estimate the cost of capital. The 2-stage dividend discount model is more suitable for investors seeking to estimate the intrinsic value of a stock, while the CAPM is more suitable for investors seeking to estimate the expected return on investment.

In conclusion, the 2-stage dividend discount model is a powerful valuation method that provides a unique perspective on the intrinsic value of a stock. By understanding the strengths and weaknesses of the 2-stage dividend discount model in comparison to other valuation methods, investors can make more informed investment decisions.

Conclusion: Mastering the 2-Stage Dividend Discount Model for Informed Investment Decisions

In conclusion, the 2-stage dividend discount model is a powerful tool for investors seeking to estimate the intrinsic value of a stock. By understanding the assumptions, advantages, and limitations of the 2-stage dividend discount model, investors can make more informed investment decisions.

Throughout this article, we have explored the concept of the dividend discount model, the 2-stage dividend discount model, and its application in practice. We have also discussed the importance of accurately estimating dividend growth rates, the limitations and potential biases of the model, and its comparison with other valuation methods.

By mastering the 2-stage dividend discount model, investors can gain a deeper understanding of the intrinsic value of a stock and make more informed investment decisions. Whether you are a seasoned investor or just starting out, the 2-stage dividend discount model is a valuable tool to have in your investment toolkit.

Remember, the 2-stage dividend discount model is not a crystal ball, but rather a framework for estimating the intrinsic value of a stock. By combining the 2-stage dividend discount model with other valuation methods and fundamental analysis, investors can gain a more comprehensive understanding of the stock market and make more informed investment decisions.

In the world of dividend investing, the 2-stage dividend discount model is a powerful tool for unlocking the power of dividend investing. By understanding the 2-stage dividend discount model, investors can gain a competitive edge in the market and achieve their long-term investment goals.